Sometimes the fast evolution of business in history can be difficult to see when you are in the middle of it.

Sometimes the fast evolution of business in history can be difficult to see when you are in the middle of it.Let's put this in a broader perspective.

Imagine 10 years ago if you were called in by a group of executives wanting to know about disruptive business models 10 years ahead.

You would tell them that in 2014, a company that does not exist in 2004, nor does it's business model exist, will acquire another company with 55 employees, which prime product is an application which can send messages among mobile phones , and the price of the acquisition will be 2.5 times the price at which Nokia is acquired by Microsoft the same year.

I am very sure that your audience would thank you for your prediction, but most likely none of them would believe you. Perhaps even more if you told them the size of the price tag.

So, like in many other cases, reality beats fantasy. The fact remains that earlier this year Facebook acquired WhatsApp for $19 billion. This is the second largest technology acquisition in history, after the HP acquisition of Compaq in 2001 for $25 billion.

Many would say that Facebook today is the world's largest communication company with close to 1.4 billion users, offering anything from voice communication over messaging to sharing of photos and download of applications.

When we compare many of the high profile acquisitions of Internet stars over the last decade, it becomes apparent that WhatsApp is standing out compared with the others. After four years WhatsApp had reached 419 million users compared to Facebook, which reached 145 million users in the same amount of time since it was launched. Twitter and Skype had reached roughly 50 million users in the same period since they were launched. Since the acquisition WhatsApp has continued to grow and reportedly reached 600 million users in August 2014, which represents an accelerated growth lately.

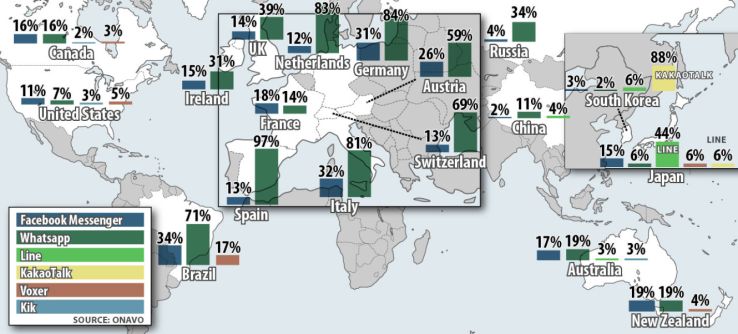

One of the things that strikes the eye when looking at the service penetration of messaging applications worldwide is that there are large differences among different countries. In countries like the United States, Canada, France and Australia Facebook Messenger seem to have to comparable penetration to WhatsApp of about 11% to 17% of mobile Internet users. In many European countries including Germany, Italy, Spain, and the Netherlands WhatsApp enjoys penetrations of 80% to 90% with Facebook Messenger on about 1/3 of the penetration in the same countries. Brazil is outstanding as a country where Facebook Messenger has a relatively high penetration of 34%, and where WhatsApp has an even higher penetration with 71% of the mobile Internet users. In any case, it becomes very clear that WhatsApp brings a lot of new messaging users to Facebook that it's Messenger app didn't reach before.

When Facebook acquired WhatsApp it had approximately 450 million users, and it has grown to 600 million users since. Not only does the number of users impress, but also the frequency by which these users actually use the app. WhatsApp enjoys a rate of 70% of its users being active on a daily basis compared to Facebook Messenger which has about 61%. This should be compared to the industry standard which is between 10% to 22% of the users.

So, at $19 billion at the time of the acquisition each WhatsApp customer was worth about $40 per user. When Facebook launched it's IPO in 2012 it was worth about $125 per user. Today, with about 1.35 billion users and a market cap of $208 billion, the company is worth $154 per user. So measured by the number of users and their level of activity it seems that the price tag of WhatsApp was reasonable. Data is the new oil, and so WhatsApp will unquestionably have access to data about content and communication that people share to an extent that was not a accessible to Facebook before the acquisition. It is however a very difficult to estimate the value of this information, but the concerns lately on privacy on the Internet could have provoked a migration to communication in smaller and more closed groups, and Facebook might have secured a significant access to the data from this type of communication going forward with this deal.

When you start to look into some of the operational metrics of WhatsApp, some remarkable numbers begin to appear: With 450 million users and only 32 engineers, it means that each engineer was serving 14 million users. This measure is quite unique compared to any other company offering software to serve its customers. It is also a remarkable to note that WhatsApp hasn't spent nothing on marketing until today. The application was spread only by a viral channels. Apparently, the company does not even have marketing or PR staff.

But there also are also other types of rationale behind the acquisition that could be interesting to look at. WhatsApp until today, does only work on mobile phones. As part of the authentication process WhatsApp will verify your phone number. This means that WhatsApp has information on the valid cellphone number of all its users. This is an information that many other application developers is trying to get from people. However, lately there has been rumors that WhatsApp might be developing a Web version. We can only speculate as to how they will do the authentication of the user's identity, but one option would be to pair the user registration with an authentication through a mobile phone.

Some analysts point to research showing that users are turning away from Facebook Messenger to other instant messaging applications such as watchApp and WeChat. It is possible that the Facebook management had seen this trends very early, and wanted to make sure our that nobody else would pick up WhatsApp. There are reports that Google was interested in acquiring the company and had offered a price tag of $10 billion. Now, according to some reports Facebook Messenger has suffered a decline from 512 million users in the first quarter of 2013 to 313 million users in third quarter 2014.

Finally, it also seem that Software based Internet companies have more appetite on large acquisitions compared to hardware based Internet companies. When comparing the acquisitions made by Facebook, Amazon, Google and Apple it appears that Facebook and Google have made much larger acquisitions over time compared to the other two.